AI Finance Transformation 2026: Real Ops Wins

I used to think “AI in finance ops” meant prettier dashboards and a chatbot that apologized a lot. Then one quarter-end close, a small AI agent caught a duplicate vendor payment before it left the building—while I was busy arguing with a spreadsheet about commas. That moment didn’t feel futuristic. It felt… embarrassingly practical. This post is my field-notes version of how AI transformed finance operations: the real results, the infrastructure it quietly demands, and the governance you can’t duct-tape on later.

From “AI pilot” to real close-week relief

My quarter-end close story: the tiny automation that stopped a duplicate payment

During one quarter-end close, we were moving fast and tired. In AP, two invoices looked “different enough” to slip through: one came from email, one came from the vendor portal. Same vendor, same amount, same date range—just a slightly different invoice number format. Before AI, we relied on manual checks and a few basic rules, and that week those checks were stretched thin.

Our small AI automation did one simple thing: it flagged near-duplicates using vendor + amount + service period, then pushed a short alert into the AP queue. That alert gave us a 30-second pause to confirm the match and stop the second payment. It wasn’t flashy. But it was real close-week relief, and it built trust faster than any “big transformation” slide.

What’s driving AI adoption in finance ops

In my experience, AI adoption isn’t driven by curiosity—it’s driven by pressure. The teams I talk to are moving because the work is not slowing down, and the margin for error is shrinking.

- Operational pressure: close timelines stay tight even as transaction volume grows.

- Talent constraints: hiring and backfilling is hard, and training takes time.

- Competitive pressure: faster, cleaner finance ops supports pricing, cash flow, and market share.

Where AI efficiency gains show up first

Based on the “How AI Transformed Finance Operations: Real Results” patterns, the first wins usually land where work is repetitive, rules-based, and high-volume:

- Accounts payable (AP): invoice capture, coding suggestions, duplicate detection, exception routing.

- Reconciliations: matching transactions, explaining variances, preparing support for reviewers.

- Collections outreach: prioritizing accounts, drafting reminders, summarizing dispute history.

A quick reality check on “15% automated”

When I hear “we automated 15% of routine decisions,” I don’t translate that to “15% fewer people.” I translate it to 15% fewer interruptions, fewer late nights, and more time for work that needs judgment—like resolving exceptions, improving controls, and partnering with the business.

Mini-tangent: the most annoying process is often the best first target

The best first AI use case is often the one everyone complains about. Annoying processes tend to be:

- Frequent (so savings repeat)

- Easy to measure (cycle time, error rate, rework)

- Full of “small decisions” (perfect for assistive AI)

In finance transformation, the quickest credibility comes from fixing the daily pain—not from launching the biggest pilot.

Digital employees in financial operations (the helpful kind)

When I say “digital employees” (AI agents), I mean software workers that can understand a goal, follow a set of rules, use approved tools, and leave a clear audit trail. They don’t “replace Finance.” They don’t get free access to every system. And they definitely don’t get to invent policy. In the source material, the real shift was not hype—it was measurable ops relief when routine work stopped piling up.

What I mean by AI agents (and what I don’t)

- Do: execute defined workflows, ask for approval when needed, and document every step.

- Don’t: act like a human with unlimited judgment, or operate without controls.

- Do: work inside guardrails (roles, permissions, templates, and compliance checks).

Agentic workflow automation: not just “a bot that clicks”

I used to think automation was mostly screen scraping and button pushing. That’s the old model: a bot repeats steps until something changes, then it breaks. An agent is different. It aims for an outcome—like “close this case” or “reconcile this account”—and can handle the steps in between.

| RPA bot | AI agent |

|---|---|

| Follows fixed clicks | Follows a goal with rules |

| Stops on exceptions | Routes, asks, or retries safely |

| Limited context | Uses context + logs decisions |

Where digital employees shine in finance ops

From what I’ve seen in real finance operations results, digital employees perform best in three areas:

- Regulated customer conversations: they can draft responses using approved language, pull account facts, and escalate anything sensitive.

- Standardized back-office processes: invoice matching, cash application, vendor onboarding, and close checklists—especially when steps are repeatable.

- Multi-step task orchestration: “collect docs → validate → update ERP → notify stakeholders” with timestamps and evidence.

Generative AI decision support (not “making up numbers”)

In FP&A, I like generative AI most as a narrative assistant: it drafts variance explanations, turns notes into clean commentary, and highlights anomalies for review. It should never be the source of truth. The numbers still come from governed systems; the AI helps me see and explain them faster.

My small confession: I was skeptical until I watched exception handling get calmer—fewer pings, clearer queues, and better handoffs when humans truly needed to step in.

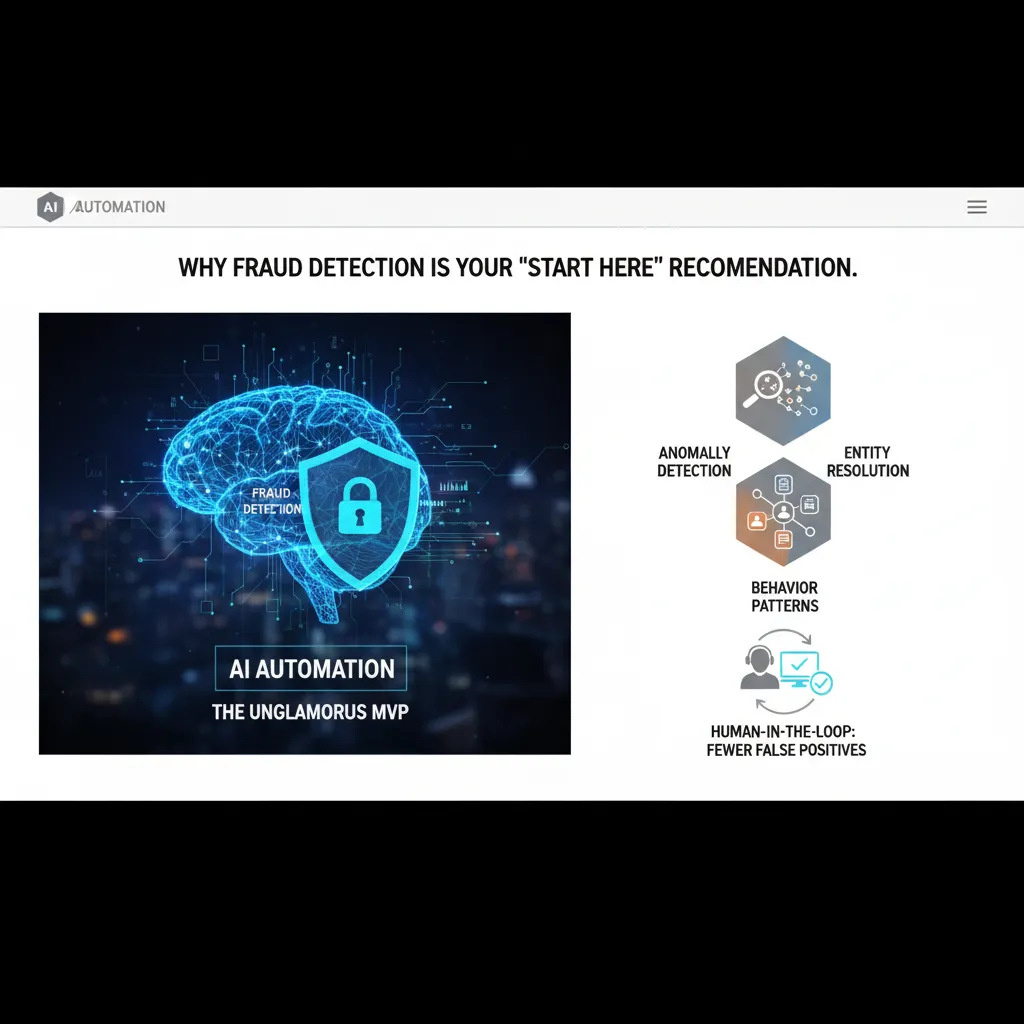

Fraud detection AI automation: the unglamorous MVP

When people ask me where to start with AI in finance ops, I often say fraud detection. Not because it’s exciting, but because it’s a safe, high-impact place to prove value. Even cautious teams can agree on the goal: stop losses, reduce noise, and protect customers. In the source story, the biggest wins came from picking a workflow that already had clear signals, clear owners, and clear outcomes.

Why fraud detection became my “start here” recommendation

Fraud work is already data-rich: transactions, device info, login history, chargebacks, and support notes. That makes it a practical MVP. I also like it because the business case is simple: fewer bad payouts and fewer hours wasted on false alarms.

- Fast feedback loops: you know quickly if alerts are useful.

- Measurable metrics: loss rate, alert volume, review time, chargeback rate.

- Low process disruption: AI can assist before it “decides.”

What AI fraud detection looks like in practice

In real operations, it’s rarely one model. It’s a system that combines:

- Anomaly detection: flags unusual amounts, timing, locations, or device changes.

- Entity resolution: links “different” accounts that share devices, emails, bank rails, or addresses.

- Behavior patterns: watches sequences like password reset → new payee → urgent transfer.

I’ve seen teams get the best results when they treat the model output as a risk score + reason codes, not a black box.

The operational win: fewer false positives with human-in-the-loop

The unglamorous part is labeling. When analysts tag edge cases—“legit but unusual,” “friendly fraud,” “merchant error”—the system learns what not to block. Over time, alert quality improves and review queues shrink.

“AI didn’t replace our reviewers. It made their judgment reusable.”

Collections and chargebacks: triage, route, and document

Agentic AI can do more than flag risk. It can triage disputes, route them to the right owner, and assemble evidence packs with compliance notes. For example:

- Detect chargeback reason + match to order and delivery proof

- Draft a response and request missing documents

- Log actions for audit and policy checks

Hypothetical scenario: voice deepfake vs biometrics + logging

A caller claims to be the CFO and demands an urgent vendor change. A deepfake voice sounds convincing. With voice biometrics, the system detects a mismatch, triggers step-up verification, and writes a compliance log:

event=payee_change; risk=high; voice_match=false; step_up=required; reviewer=assignedThe result is simple: fewer panic-driven approvals, and a clean trail for auditors.

Regulatory compliance AI governance (the part I wish I’d done earlier)

In my finance ops AI rollout, the biggest lesson was that regulation is no longer “nice guidance.” It’s moving fast toward enforcement, and that changes how you plan. When rules were softer, we treated governance like documentation we could catch up on later. That was a mistake. Once auditors and risk teams expect proof, your timeline needs room for controls, reviews, and evidence—just like any other finance process.

Regulatory momentum: guidance to enforcement

What I saw in practice: regulators and internal compliance teams started asking not only what the model does, but how it was trained, monitored, and approved. That meant our “pilot” had to look like a production system earlier than expected. If you wait, you end up rebuilding workflows, redoing access rules, and re-running validations under pressure.

My “three-binder” checklist

I now keep a simple governance pack—three binders (digital folders) that map to how finance leaders think: controls, monitoring, and auditability.

- Data governance: data sources, ownership, retention, PII handling, and who can change mappings.

- Model monitoring: drift checks, accuracy thresholds, exception queues, and incident response.

- Approvals & audit trails: sign-offs, change logs, prompt/version history, and evidence for audits.

Responsible AI governance in finance ops

From the “How AI Transformed Finance Operations: Real Results” playbook, the wins came when we treated responsible AI like a control framework, not a slide deck. I built four required checks into every workflow:

- Bias checks and discrimination prevention (especially for credit, collections, and vendor decisions).

- Explainability: a clear reason code for outputs that affect money movement or reporting.

- Transparency: users can see data inputs, assumptions, and confidence levels.

- Human-in-the-loop for material decisions and close adjustments.

Stopping generative AI from becoming “creative accounting”

Generative AI is great for decision support, but it can also “fill gaps” in ways that look like earnings management. My rule: GenAI can draft, summarize, and suggest, but it cannot post. We enforced this with workflow gates and hard controls:

- Only structured systems can create journal entries; GenAI outputs are non-posting notes.

- Every suggestion must cite source transactions or policies.

- Exceptions route to a reviewer with an audit trail.

What’s changing enterprise AI: standardization, interoperability, and MCP

Governance is getting more feasible because enterprise AI is becoming more standardized. Interoperability patterns—and MCP (Model Context Protocol) style connectors—make it easier to control tool access, log prompts, and centralize policy enforcement across models. Instead of building one-off controls per vendor, we can apply consistent guardrails across the stack.

Cloud maturity + real-time connectivity: the boring stuff that makes AI work

In our finance ops AI work, I learned fast that models don’t fail first—plumbing does. We had strong use cases from “How AI Transformed Finance Operations: Real Results,” but the wins only showed up when our cloud and connectivity stopped being “good enough” and became reliable, fast, and secure.

Cloud maturity in financial services: why lift-and-shift didn’t help my AI roadmap

Our first move was a classic lift-and-shift: move old apps to the cloud and call it progress. It helped with data center pressure, but it didn’t help AI. The data stayed in silos, batch jobs stayed slow, and teams still fought over access. AI needs clean data paths, shared services, and repeatable deployment—not just new hosting.

Real-time connectivity (low latency): the hidden requirement

Fraud detection, pricing updates, and customer experience all depend on low-latency signals. If events arrive late, the “smart” decision arrives late too. We saw that real-time connectivity was not a nice-to-have; it was the difference between stopping a risky transaction and writing a post-incident report.

- Fraud: decisions must happen in milliseconds, not minutes.

- Pricing: rates and limits need fast refresh to avoid leakage.

- Customer experience: fewer false declines when context is current.

AI acceleration infrastructure needs: GPUs, queues, observability, and cost controls

Once we pushed for real-time, we had to build the boring stack that keeps AI stable:

- GPUs for training and some inference workloads.

- Queues/streams to handle spikes without dropping events.

- Observability (logs, metrics, traces) to see drift, latency, and failures.

- Cost controls because runaway inference calls can burn budgets fast.

We treated cost like a feature: budgets, alerts, and simple rules like auto-scale down after peak.

Enterprise-grade AI integration: interoperability, security, and access management

Finance ops lives inside a web of ERP, CRM, payment rails, and risk tools. AI had to fit that reality with interoperability, strong security, and tight access management. Role-based access, audit trails, and data masking weren’t optional—they were the price of production.

AI without plumbing is espresso poured into a leaky paper cup.

Putting it together: a scrappy transformation strategy (with ROI sanity)

When I look back at the real ops wins from “How AI Transformed Finance Operations: Real Results,” the pattern is simple: the teams that moved fastest didn’t start with a big platform rebuild. They started with a small, repeatable loop that kept risk under control and made ROI easy to see.

My finance services transformation strategy: 1 outcome, 1 workflow, 1 risk owner

I keep the first move almost boring. I pick one outcome (like faster close, fewer exceptions, or better collections), then one workflow that drives it (invoice matching, reconciliations, dispute handling, KYC refresh), and then one risk owner who can say “yes” or “stop.” That risk owner is usually Finance Ops + Compliance together, because AI in financial services fails when ownership is split.

ROI financial services implementation: where savings actually come from

I don’t sell ROI with vague “productivity.” I track where savings really show up in finance operations:

- Time: fewer touches per case, shorter cycle time, less rework.

- Errors: fewer misposts, fewer duplicate payments, cleaner master data.

- Leakage: missed fees, unbilled items, write-offs that should have been prevented.

- Faster decisions: quicker credit holds/releases, faster dispute resolution, better cash forecasting.

If I can’t tie the AI workflow to at least one of those, I treat it as a demo—not a transformation.

Agentic AI enterprise scale: when to scale vs when to pause

Agentic AI is powerful, but I only scale when I see stable signals: consistent accuracy on edge cases, clear audit trails, low override rates, and no spike in downstream exceptions. I pause when the model “looks right” but can’t explain itself, when controls are manual, or when teams start building workarounds. In finance, quiet failure is the expensive kind.

Customer-side bonus: generative AI customer experience + voice AI customer support

On the customer side, I like generative AI for customer experience and voice AI customer support when it’s responsible: clear disclosure, secure data handling, tight knowledge sources, and an easy handoff to humans for billing disputes, hardship, or fraud. Done right, it reduces call volume and speeds answers without creating new risk.

My takeaway for 2026 is that AI reshaping financial services is less about magic—and more about disciplined repetition: pick the next workflow, measure the real savings, tighten controls, and only then scale.

TL;DR: AI is moving from experiments to regulated, enterprise capability in finance ops. Agentic AI and digital employees are driving measurable efficiency and productivity, fraud detection is a breakout use case, voice AI is rising fast, and responsible AI governance + cloud maturity + real-time connectivity are now table stakes for scaling safely in 2026.

Comments

Post a Comment